Ciao , sei nel profilo di Gabriele Dado’. Visualizza tutte le Isole i cui lavora, le sue attività e i suoi asset. Potrai avere inoltre una visione su tutti i i post che ha pubblicato. Tutti i dati presenti in schermata sono automatizzati e si alimentano in base alle attività che l'utente effettua su HUI (esempio ToDo ultimate, unit delle attività...)

It is my pleasure to share the exciting news that BLK has been selected as the winner for Scotland Prestige Awards!

BLK Wins the 2022 Scotland Prestige Awards

This is in recognition of the massive work we have done especially in support of local Scottish businesses, enabling them to source directly from suppliers and cut their supply chain costs as well as carbon footprint.

The Scotland Prestige Guide will be available to over 500,000 subscribers on a national basis. It will also reach over 100,000 readers located in Scotland and surrounding regions in both print and digital formats. Copies will be sent directly to businesses and homes across the region.

Each year the organisers invite both readers and contributors to the Corporate Livewire and LTG publications to put forward companies, products, services and individuals who they feel are deserving of recognition. Each nominee is reviewed by a panel of judges who ultimately pick a winner in each area.

"We are proud to support the local economies, sourcing directly and streamlining their costs, especially in these difficult times where inflation and cost of raw materials is driving prices up across the board, challenging businesses’ very viability. By allowing local businesses reduce their procurement cost, we have a direct impact on thousands of families across Scotland and the UK and we are privileged to be able to do our bit to ensure local business continuity and growth"

Welcome to BLK Shipping, our regular update from the shipping market. In this issue, we’ll be covering:

Wet Cargo

Dry Cargo

Containers

Gas

Subscribe to our newsletter to stay up-to-date with our Shipping Weekly and follow us on Facebook and LinkedIn to never miss an update.

Wet Cargo

The increasing price of crude oil has been driving the tankers’ charter rates up, although the availability of VLCCs meant a general slowdown for this segment.

VLCC – Very Large Crude Carriers saw a decline over the past week, primarily due to the oversupply of tonnage in the market. Outlook: Stable

Suezmax – strong rally Sith over 1800% increase WoW for suezmaxes, with a very strong performance, especially in the Mediterranean. Outlook: Positive

Aframax – afra rates more gained ground, with a general strengthening across most routes. Outlook: Positive

Dirty Products – Apart from the usual busy market in the Med and Black Sea, demand remained weak in all other regions, causing rates to soften. Outlook: Stable.

Clean Products – Charter rates weakened across the board with some routes losing over 50% WoW. The MR market remained relatively oversupplied, and the lack of available cargoes did the rest to cause charter rates to slip by an average of 10% Outlook: Negative

MR – weakening demand did not support the MR rates, which, coupled with the oversupply of carrying capacity in the market, caused rates to fall across the board. Outlook: Negative

LR1 –demand for log-range tankers fell in the last few weeks and continues on a downward trend. Outlook: Negative

LR2 –LR2 tankers weakened approx. 20% WoW but, on average, remain still strong compared to this summer. Outlook: Stable

Handy –Handy earnings weakened too, returning below $3500/day and losing all the ground gained in September Outlook: Stable

Dirty Panamax – Rates softened on most routes, bringing Panamax rates down 22% compared to last month. Outlook: Negative

Dry Cargo

Strong performance for the bunkers on most routes and across all segments, with rates at their highest levels in over 10 years.

Capesize – Capes grew up to 30% in the last week, averaging nearly $73k/day and rates climbing sharply to unchartered heights. Outlook: Positive

Panamax – Still another good week for the panamaxes, although slightly in decline on the Atlantic and on the routes Indonesia to China. Outlook: Positive

Supramax – Supramaxes lost ground in recent days, after climbing steadily over the course of 2021. The second half of September saw relatively steady rates, settling on an average of $30k/day Outlook: Stable

Handysize – Handy market still performing very well. After a strong July-August rally, a slow-down in September now it settled on $36k+/day with short voyages routes fetching over $40k/day. Outlook: Stable

Container

Container rates finally found some market resistance, with Neo-panamaxes vessels finding difficult to push much above the $145k/day mark.

Backlogs in major ports are gravely disrupting supply chains, with queues of over 70 container vessels at Long Beach and other major ports in the US, Europe and China.

We are now seeing, as predicted, a decrease in smaller-batches shipments westbound from Asia to Europe, accompanied by a subsequent easing of the TEU rates which now came down on the high $8000s mark.

Outlook: Stable

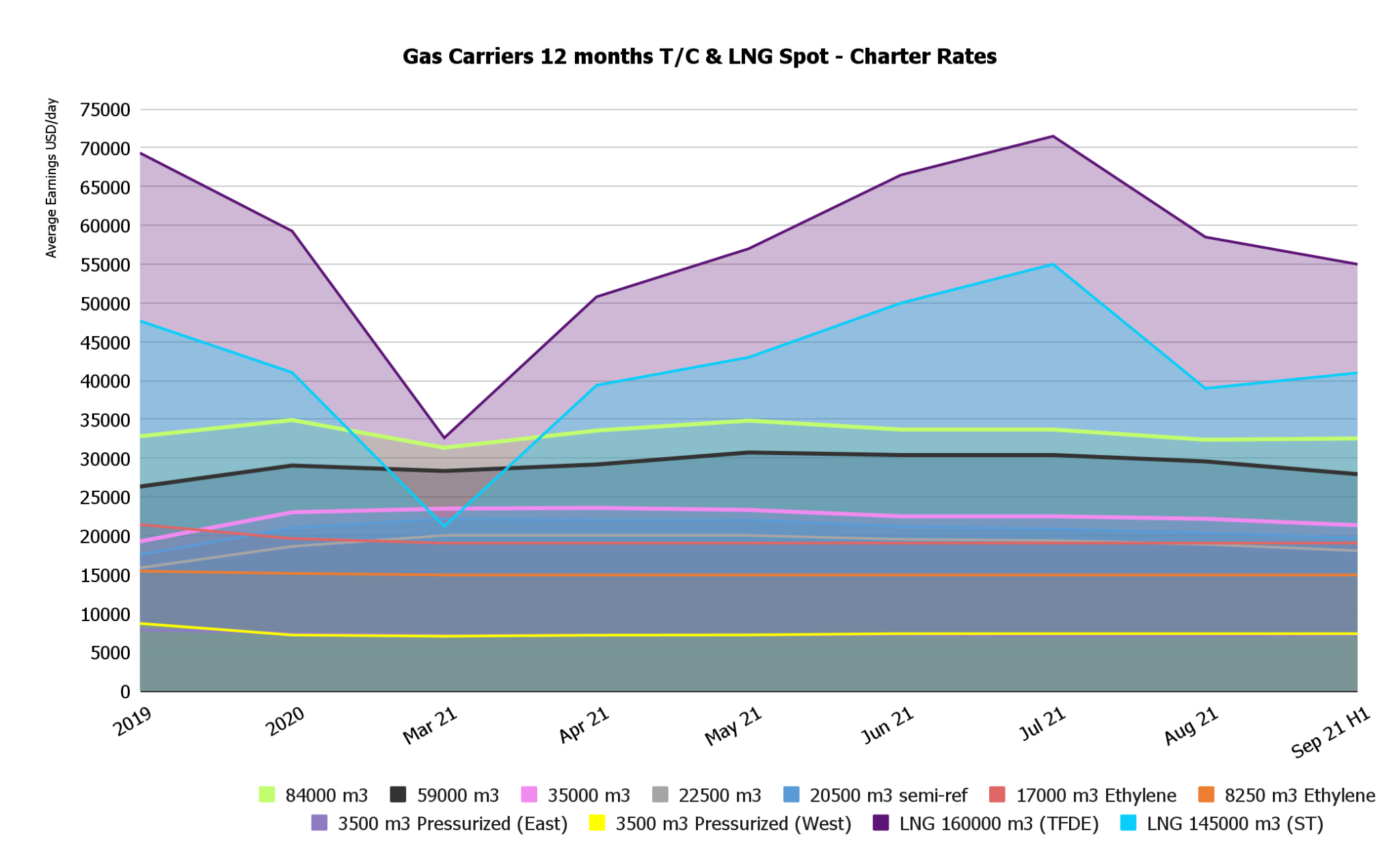

Gas

Rates for Gas Carriers remained picked up strongly, driven by the strong demand for gas worldwide and the surge in gas prices across Europe and North America.

Pressurized and semi-pressurized vessel rates remained constant, whilst the biggest winners appeared to be LNG carriers, with rates now nearing the $85k/day for 160000 m3 vessels.

Outlook: Positive

To learn more about how we can support your business shipping as cheaply and environmentally-friendly as possible, visit us at BLK.

Subscribe to our newsletter to stay up-to-date with our weekly shipping updates.

Did you miss our previous shipping article? Read it now.

In this article we will look at the crude oil price forecast and its impact on fuel prices. In 2022, EIA expect an average of about $66/b for crude, but traders, believe that oil may break through $100/b, nearing the $120/b by the end of 2022, which paints a grim pictures for fuel-reliant businesses.

Price Composition of Distillate Fuels

The price that final users pay for petrol, diesel, jet fuel and, in general, distillate fuels is governed by the local wholesale fuel price. This are affected by:

the global price of crude oil

supply and demand for crude

world refinery production and capacity

currency exchange rate, as refined fuel is sold in USD

distribution costs

arbitrary gross margin retailers decide to introduce

fuel duty charged by the local government (57.95p/l in the UK)

VAT/GST/value added tax (20% in the UK)

While some of these stay largely static – such as the fuel duty rate and VAT – others such as the oil price and dollar to local currency exchange rate can be very volatile.

The chart above looks at the pump price of petrol and diesel (top), together with the underlying wholesale prices (bottom) for the United Kingdom.

The ‘Rocket & Feather’ Effect

This is the dynamic according to which fuel prices always appear to rise faster than they come down, i.e. they go up like a rocket but fall like a feather.

Whenever the price of crude (and, in turn, that of wholesale fuels) goes up, retailers see their margins eroded very quickly and therefore have to take immediate action to bring the pump prices up in order to preserve their bottom line.

When crude oil price comes down, however, retailers’ margin suddenly widens and stays higher for as long as they maintain the current pricing level.

This explains the general reluctance to fall back in line, in order to hold on to their earning as much as possible, before being driven down by the competition and the inevitable law of supply and demand.

How low can fuel prices go?

There is a limit to how low prices can go and this is the fuel tax, depending on each specific country.

Realistically, there is another 10% above the tax that accounts for distribution, from the oilfield to the pump (that is provided that retailers and oil majors give fuel away for free). In the UK, fuel duty is set at 57.95p/l, plus VAT on the total price make up for the vast majority of the price people pay.

When the price of oil is falling it can also create a perception that pump prices are not reducing as much as they should because the lower the pump prices falls, the greater the percentage of tax.

Look Ahead

Brent prices have risen over the past year as result of steady draws on global oil inventories, which averaged 1.8 million barrels per day (b/d) during the first half of 2021.

From August to October, crude oil price raised 45% and we expect prices to continue to climb during the fourth quarter of 2021.

Brent Crude prices 2021

In 2022, we expect that growth in production from OPEC+, US and other non-OPEC countries will slowly outpace the growth in global oil consumption and contribute to Brent prices declining to an annual average of about $66/b.

In the short term, however, fuel-reliant businesses such as haulers, airlines and costal shipping companies, are exposed to a significant risk, with the price of assets’ OPEX eating into their margin.

Despite the cautious optimism of the EIA, traders believe that the price of crude may break through $100/b, nearing the $120/b by the end of 2022.

In this scenario, however, we need to keep into account that the price of futures is also influenced by a certain “risk factor” (in other words, traders factor in the risk they are going to assume by agreeing to purchase at a specific price at a later date) as well as a certain “margin” they are expecting to make. While the two items may balance each-other out, the upper interval still paints a grim picture for consumers and energy-reliant businesses, which will be called to face uncertain times as we venture into an uncharted territory following the COVID pandemic.

Mitigating the Risk Ahead

Remember to look at the spot market whenever in need for fuels.

Blkcommodites.com is the online spot market, where you can find pre-vetted suppliers from around the world to purchase at be best possible prices, below the institutional markets.

The reason being BLK leverages its expertise in supply chain management and aggregate volume from multiple buyers all over the UK, Italy and the rest of Europe to negotiate ad hoc deals with suppliers, coming 4-5% below the Platts’ price for distillate fuels.

Take immediately advantage of our negotiated $20/ton discount on the Platts NWE FOB and get in touch today for any specific requirements (e.g. jet fuel, LPG, etc.).

Check-out our negotiated rates for diesel or get in touch and secure your business from fuel prices’ fluctuations leveraging the purchasing power of hundreds of players like you, already purchasing on Blkcommodities.com.

Delighted to have been nominated for the #SMEFinanceAwards 2021!

At BLK we are committed to bringing down barriers and allow businesses to buy directly from producers, wherever they are in the world.

#SMEs make up the backbone of our #economy and enabling them to cut their variable costs by #sourcing directly from producers, without middle men, means higher margins and more #competitively on international markets.

We are passionate about opening and #digitalising #markets and the SME Finance Awards nomination is a great testimony that we’re on the right track - thanks to you all!

Welcome to BLK Shipping, our regular update from the shipping market. In this issue, we’ll be covering:

Wet Cargo

Dry Cargo

Containers

Gas

Subscribe to our newsletter to stay up-to-date with our Shipping Weekly and follow us on Facebook and LinkedIn to never miss an update.

Wet Cargo

Oversupply of carrying capacity in the market counterbalanced significantly the rising price of oil and the tanker rates kept dropping across the board, with the only exception of VLCCs

Crude Tanker Spot Charter Rates

VLCC – Very Large Crude Carriers were the only vessels with a strong performance, given their direct link to the crude trading. China routes were the busiest with a 3.5 times increase WoW. Outlook: Positive

Suezmax – rates weakened on all routes with the only exception of the Indian Ocean, where Suezmaxes did 9% better than the previous week. Outlook: Stable

Aframax – the Med remained the only area where Aframaxes keep performing, with a general, continued declined that went on throughout September. Outlook: Stable

Crude Tankers Spot Charter Rates

Dirty Products – Relatively busy in the Mediterranean, whilst demand remaining weak in all other regions, with a marked oversupply of carrying capacity. Outlook: Negative.

Clean Products – Charter rates weakened across the board, especially for short voyages. Outlook: Stable

Product Tanker Spot Cargo Rates

MR – uptake in demand did not have the expected positive effects on MR rates, owing to the oversupply of carrying capacity in the market. Outlook: Negative

LR1 –demand for log-range tankers fell in the last few weeks. Outlook: Negative

LR2 –continued decline in LR rates would appear to continue on this trend as plenty of vessels remain unemployed. Outlook: Negative

Handy –Handy earnings bounced back below $4000/day with a weakened performance on all routes except the Med. Outlook: Stable

Dirty Panamax – Rates continued softening pretty much all routes, with a recorded drops up to 30% WoW. Outlook: Stable

Product Tanker Spot Rates

Dry Cargo

Bulk carrier rates rallied during the past week with a market “on fire”and at its highest since 2008. WoW growth recorded up to 44%, pushing capesize rates beyond $60k/day on some routes.

Bulk Carrier Spot Cargo Earnings per day

Capesize – Capes were the strongest performers in a very active market, characterised by a strong demand and an undersupply of carrying capacity Outlook: Positive

Panamax – Still another good week for the panamaxes, with an average growth of 5% across the board and a decisively positive outlook. Outlook: Positive

Supramax – Supramaxes remained relatively stable, with recorded variations up to 3% and average rates just north of $31,500/day Outlook: Stable

Handysize – small-sized bulkers did relatively well in the past couple of weeks, with a continual growth now averaging $34k+/day and voyage charters smashing through $40k/day on South-American routes. Outlook: Positive

Bulk Carrier Spot Charter Rates

Container

Container rates finally look like they’re stabilising, with Neo-panamax vessels settling just above the$145k/day mark and container prices on the routes China-Europe recording an inflexion for the first time in months.

Container Vessel Average Earnings per TEU per day

On the raw materials side, however, and especially in chemical commodities, the high freight rates keep impacting prices of goods to the extent that it is equivalent or cheaper to source from European suppliers.

This has led to a decrease in smaller-batch shipments westbound from Asia to Europe which, together with the ongoing raw material shortage and increase in prices of Chinese factory outputs, provoked a subsequent easing of the TEU rates. We should continue seeing this trend toward the end of the year and possibly into 2022.

Outlook: Stable

Container Vessel Charter Rates

Gas

Rates for Gas Carriers remained declined slightly, with a 18% hit suffered by for 145,000 m3 LNG Carriers.

Gas Tankers Cargo Rates

This was expected as plenty of tonnage was tied-up in dock for ballast water treatment systems installation and is now slowly coming back into the market, increasing overall supply. Outlook: Stable

To learn more about how we can support your business shipping as cheaply and environmentally-friendly as possible, visit us at BLK.

Did you miss our previous edition of BLK Shipping? Check it out!

Subscribe to our newsletter to stay up-to-date with our weekly shipping updates.

Welcome to BLK Shipping, our regular update from the shipping market. In this issue, we’ll be covering:

Wet Cargo

Dry Cargo

Containers

Gas

Subscribe to our newsletter to stay up-to-date with our Shipping Weekly and follow us on Facebook and LinkedIn to never miss an update.

Wet Cargo

The increasing price of crude oil has been driving the tankers’ charter rates up throughout July, although this has now slowed down and we are seeing a further downward trend in rates.

VLCC – Very Large Crude Carriers remained pretty much stable. Although we’re still unbelievably far from 2019 levels, we can now see positive signs of pick-up. Outlook: Stable

Suezmax – rates remained still, apart for a few routes where we saw a near 100% growth. As the oil price stabilises, we expect that the vessel charter rates will go with it. Outlook: Stable

Aframax – afra rates more lost ground, with a general weakening across most routes. Outlook: Stable

Dirty Products – Relatively busy in the Mediterranean, whilst supply and demand remaining weak in all other regions. Outlook: Stable.

Clean Products – Charter rates weakened across the board with some routes losing over 70% WoW.. Outlook: Stable

MR – uptake in demand did not have the expected positive effects on MR rates, owing to the oversupply of carrying capacity in the market. Outlook: Stable

LR1 –demand for log-range tankers fell in the last few weeks. Outlook: Stable

LR2 –Good rally for LR2 tankers, up to 20% surge in a week. Outlook: Positive

Handy –Handy earnings bounced back up above $7000/day and it looks like the beginning of a positive performance. Outlook: Stable

Dirty Panamax – Rates continued softening very slightly on all routes, with a general 1% – 5% drop since last week. Outlook: Stable

Dry Cargo

Slow-down on most routes and across all segments, although bulkers remain pretty strong compared to 2019 and 2020 performance.

Capesize – Capes declined between 5 to 20%, having broken through the $40k/day for the first time in years and now travelling on $41k+/day for scrubber-fitted vessels. Outlook: Stable

Panamax – Still another good week for the panamaxes, although slightly in decline compared to the last week of August. Outlook: Stable

Supramax – Supramaxes lost ground in recent days, after climbing steadily over the course of 2021. The second half of August and early September saw a reduction of 4-7% to settle on an average of $35k/day Outlook: Stable

Handysize – the biggest fluctuations happened within the Handy market. Still high after a strong July-August rally, now it fell slightly to $32k+/day mark. Outlook: Stable

Container

Container rates seem unstoppable, with 4400 TEU vessels now nearing the $100k/day mark themselves. Neo-panamax vessels are now close to the $145k/day mark, with a significant impact on the economy of most western countries coming out of the pandemic.

On the raw materials side, however, and especially in chemical commodities, the high freight rates (now looking upwards of $20,000 per TEU on the route China – Europe) now impact prices of goods to the extent that it is equivalent or cheaper to source from European suppliers.

We expect to see a continual decrease in smaller-batches shipments westbound from Asia to Europe, hopefully accompanied by a subsequent easing of the TEU rates towards the end of the year.

Outlook: Positive

Gas

Rates for Gas Carriers remained declined slightly, with the biggest hit suffered by for large carriers 145,000 m3 and above. Pressurized and semi-pressurized vessel rates remained constant.

This was expected as plenty of tonnage was tied-up in dock for ballast water treatment systems installation and is now slowly coming back into the market, increasing overall supply. Outlook: Stable

To learn more about how we can support your business shipping as cheaply and environmentally-friendly as possible, visit us at BLK. Subscribe to our newsletter to stay up-to-date with our weekly shipping updates.

QUALITY – COST – SERVICE DELIVERY ARE THE FOUNDATIONS OF OUR RATING CRITERIA.

Here’s how we specifically assess “Cost”.

A supplier background check must go beyond the mere credit report, which is readily available for the vast majority of the business anyway and does not give a true reflection on the actual operational profile of a company.

Standard credit reports fall very short of evaluating a business’ quality, its positioning in relation to cost and, most importantly, service delivery.

For this reason, BLK has developed a proprietary evaluation method, currently used as a reference standard within the commodity trading and chemical manufacturing industries and validated on hundreds of clients already.

The BLK Rating, which covers in detail not only financials but Quality, Cost and Service Delivery, with a deep scrutiny on companies’ environmental footprint as well, paints a comprehensive picture of a business’ real position and capabilities.

In this article, we’ll look specifically at how BLK assesses Cost to build the overall company rating.

Cost is a mix of multiple factors. It’s not merely “how expensive (or cheap) is the specific product (or quote)”. It’s about a business’ overall approach to pricing and its positioning in respect to that.

1. Average gross margin

The first item we look at when evaluating cost is the company’ average gross margin in the past 3 years. This gives a good indication on whether the company falls within the average for the industry, above or below, and in which quartile.

An average, constant gross margin in the bottom quartile, means that the company is positioned aggressively in respect to pricing and therefore not only the specific product, but their whole range is likely to be competitive in absolute terms.

2. Price vs platform

It is also important to look at the price of the specific commodity compared to those of other suppliers on BLK.

We pride ourselves of being the “Online Spot Market” and as such we drive strong price competition from vetted suppliers all over the world. A company’s price may be competitive for a specific country but fall short when compared to that of overseas competitors.

We take into account the global landscape, giving buyers a feel of how the supplier stacks up internationally.

3. Average price vs index

To complement that, we also compare the specific price of goods to that of the commodity index (whenever applicable).

This way, we get the full picture, not only via the benchmark with the rest of the private market but with the institutional one as well, comparing the BLK supplier rates’ with those achieved by the movers of huge volumes such as investment banks and blue chip trading houses.

4. Credit Terms

It’s not just about “how much does it cost” but also “how much flexibility do I have for my payment”.

Suppliers that offer credit terms and payments in instalments as opposed to pre-payment only, are ranked higher than those who don’t.

BLK acts with a buyer-centric approach and the easier supplier make for a buyer to purchase, the higher it speaks of their credibility and cost positioning.

5. Price for Specific Order

Finally, we look at the specific quote or price and evaluate it with our team of expert category managers who assign a rating on the basis of their expertise in the international landscape, market conditions and supply-demand knowledge at the specific point in time.

6. Fixed vs Variable Cost Ratio

The ratio between fixed and variable costs for the company gives an indication of how heavy the company’s specific cost base is (in relation to their cost of sales). If the Fixed/Variable costs ratio is relatively low, it underpins a strong dependance from raw materials and possibly a conservative approach to margin.

These are indicators that the company tends to be more competitive than average, and the benchmark with the index and platform average prices for the same commodity, give the full assessment on how aggressive on pricing the supplier actually is.

To find out more on how we assess quality, check out our detailed post.

Do you want to get a freeassessment of your company to understand how you position in respect to Quality, Cost, Service Delivery and how you stack-up against your direct competitors?

I provided visibility on a few of the BLK key metrics, ahead of EIE21.

These metrics are intended to give prospective BLK investors an accurate overview of the company’s operational KPIs so as to facilitate an investment decision.

Further, the graphs will showcase the HUI platform to UK investors - who will be able to contact me for any information on both companies.

The information displayed would normally require a qualified investor account and will therefore be visible only for a limited period of time. Graphs and KPIs will be visible only until Wednesday 16th June 2021 23:59.

Just sharing the good news that came this evening: we successfully onboarded a new buyer, closing a strategic procurement deal with Indulatex Chemicals SA.

Indulatex is a Portugese chemicals and latex manufacturing corporation. As part of the deal, BLK will be procuring on their behalf 4 key chemical commodities that they need to manufacture their finished performance chemicals.

I will update you shortly as soon as I have confirmation on the volumes and associated turnover.

First PO in from Cosmochem. Waiting for the signed contract this week as well.

The PO is for 2 samples from two different suppliers, needed to assess the quality of the product before placing further orders. Expected around 600 MT of caustic soda in 2021, approx 305k EUR.

This week BLK is launching a tender for the procurement of various fuels on behalf of its partners. BLK Trading is a division of BLK Global Ltd. specialising in providing supply chain solutions to customers across multiple industries.

BLK aggregates the purchasing volume of multiple buyers across various industries, conducts supplier vetting, assessment and negotiations on behalf of our partners and arrange spot and/or long-term supply deals on the basis of its proprietary evaluation criterion based on Quality – Cost – Service Delivery.

BLK aims to deliver best-in-class services to key industry players at market-leading rates. With these premises, BLK wishes to tender for the supply of 500,000 MTof various fuels, including but not limited to Diesel EN590, Petrol/Gasoline EN228, Jet A-1 DS 91-091, Aviation Biofuel, Biodiesel EN14214, LPG EN589 and others, which are to be purchased by the BLK’s buyer pool through BLK’s proprietary platform blkcommodities.com.

Bids must be delivered electronically on or before the 31st of May 2021 at 12:00 UTC, at which time the submissions will be opened in the presence of those tenderers’ representatives who may wish to attend.

If you wish to take part to this tender, please reply with your expression of interest to this email by Wednesday 13th May 2021 at 16:00 UTC. Upon reception of the expression of interest, tenderers will receive a confidential tender pack electronically.

This is a great opportunity for traders, majors and producers wishing to expand their reach and customer portfolio within the Med area and the UK.

We look forward to receiving your bid and working together as strategic partners going forward.

Yesterday I completed the pitching workshop organised by Informatics Ventures for EIE21. I can also confirm they selected 30 tech companies this year from the whole of the UK, so a huge well done to BLK for making the cut!

I attached a handout from the session with tips and best practices on pitching virtually - copy of this will also be available under "Selling Tips" in the Sales app.

I’m delighted to announce that BLK won the qualifiers once again and was shortlisted to take part in EIE21 for the second year in a row.

Organised by Informatics Venures EIE is an event taking place annually, selecting the top 50 most innovative start-ups in the UK for a final showcase to various investors, ranging from Angels to VCs.

I’d like to extend my sincerest thanks to @Alex @Nima, as well as @Luigi & the EI’s team for the powerful sprint they’re giving us in 2021!

-------------

Good Morning Gabriele,

I’m delighted to inform you that you have been successful in securing a place at EIE21, which will take place on our virtual platform on Thursday 10th June 2021.

This offer is conditional upon you formerly accepting this offer, and attending and participating in all the required elements of the EIE21 Preparation Programme, which will take place online.

I would be grateful if you could now let us know the following by return, or by no later Close of Business today, Monday 15th February:

Your acceptance of the offer of a place within the EIE21 Company Cohort

Your attendance at the Bootcamp, which will take place online on 3rd March 2021. (you will be emailed further details about the event once you have accepted the offer).

Your attendance at one of the half-day Presentation Skills workshops held in March, , either in a Morning or Afternoon session. These will take place between 16th-18th March.

Your attendance at the Countdown event on 20th April 2021.

I look forward to hearing from you shortly on this.

Please contact me directly if you have any questions.

Siamo ormai su HUI da un paio di settimane ed ora che stiamo iniziando ad ambientarci volevo mettere a disposizione della comunità alcuni skills acquisiti del corso della mia carriera sperando che possiate trarne beneficio.

Volevo quindi sondare le acque per capire se ci fosse interesse nel fare dei "Sales Workshops" dove trattare delle seguenti tematiche:

Sales Fundamentals

Objections Handling

Consultative Selling

How to Close

Sales Calls

High-impact presenting

Negotiation Techniques

Se interessati, commentate pure sotto - se siamo abbastanza possiamo organizzare diverse sessioni nelle settimane a venire o a gennaio 2021.

Colgo l’occasione per fare a tutti voi i migliori auguri di Buone Feste e augurarvi un fantastico inizio del 2021!

Choose ’Continue and Reload’ to reflect the value (logic) in application.

Thanks to our 15 years of experience in the global startup ecosystem, we have identified the 6 key success factors of any company: Concept, Competence, Capital, Connection, Commitment, Creation.

Eu fugiat do anim non sit ullamco in Lorem. Duis labore sint exercitation veniam laboris culpa nisi ullamco aliqua et ad eu enim aute nostrud officia consequat. Eiusmod consectetur reprehenderit do in laborum qui mollit exercitation sint ad cupidatat ex proident id nisi ipsum.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)